Note: When I first made this article in 2018, it was full of fun little anecdotal SNAFUs, so that you could follow along and experience my travails vicariously, in an orgy of schadenfreude. But a lot has changed in the last four years, and I’ve updated the article to be much more streamlined. I’ve tried to keep the original whimsy in the introduction…

So you’re convinced. Bitcoin and cryptocurrency are the wave of the future (or at least you hope to make a fortune trading the swings), but the new tax law that you’re supposed to calculate your gain and pay taxes on every trade is cramping your style. Well, you could avoid paying taxes if you owned and traded the cryptocurrency inside of a tax deferred retirement account (or better yet, a Roth IRA so you never pay taxes on the gains).

But doing so is a bit complicated. For years I had heard of “self directed” IRAs that allowed you to invest in real estate (but my IRA didn’t have enough money to do that). Later on, I learned about how you could invest in gold through an IRA or the IRA could even start its own LLC that you manage (also known as a checkbook IRA). But I never had a reason to want to do so.

Enter Cryptocurrency. No matter whether you’re HODLing, trading, or running masternodes, the potential upside is enormous, and you don’t need a huge amount of money to get started. Now there’s a reason to put that arcane knowledge to use. What follows below are the things I’ve learned by doing this process myself.

Overview of the IRA/LLC process

First you’ll need a self directed IRA with a trust company that allows IRA/LLCs also known as checkbook IRAs. So find one with minimal fees that you trust, and open an account.

Find an attorney who specializes in this sort of thing to create your LLC.

Once your LLC is created you need

Request a bank check sent to your house from the IRA in your LLCs name

Open a bank account in your LLCs name.

Open an a corporate account for the LLC on a crypto exchange.

Wire the money from the bank account to Gdax.

Trade your heart out.

It doesn’t sound that hard, but it will likely take you several weeks to make it all the way through the process. I’ve tried to help you make it as streamlined as possible

Step 1: The first step is to open a self directed IRA

You’ll need to open a self directed IRA with a custodian that allows IRA/LLCs. My personal preferences are:

Custodian has an online sign up (I HATE paper forms)

Low fees

Allows you to pay maintenance fees with a credit card

Due to anti-kickback laws, no professional you deal with can “recommend” a service to you. So if you already selected an attorney, they can’t recommend an IRA custodian, and vice versa. But perhaps if you worded your question in the form of “which companies are the easiest to work with?” they might be able to answer.

Back in 2018, Based on these two criteria, I originally selected Kingdom Trust, updated fee schedule it looks like they eliminated the IRA/LLC option, and the regular self directed IRA option has a percent of portfolio based fee, which simply doesn’t work for me. So I ended up going with IRA Trust Services, which underwent a name change (and acquisition?) to ForgeTrust.

Fast forward to 2022, and I chose DirectedIRA. Slightly lower fees, and they can actually handle the LLC formation and be your registered agent, so they can be a one stop shop. Directed IRA is Mat Sorensen’s company (the attorney whose video above got me into this whole thing in the first place.

They’re pretty much all going to charge an annual (or more often) maintenance fee, check fee, wire fee. They often charge per “asset” within the IRA, but the only asset should be the LLC you’re going to form.

Action steps:

Fill out the Application for new account form

You need to fund the account in some way. Ideally a large chunk, like say $5000 or more, but whatever you can do that they will accept will work. You can also transfer assets from an existing IRA/Roth IRA. You can also rollover your 401k if you leave your job.

Step 2: Have an attorney form your LLC

You can begin this step while you’re waiting for the IRA to fund. I consulted with two attorneys (Mat Sorensen and Nick Spradlin). I ended up going with Nick Spradlin mainly for the lower price and because he has offices in Florida. This step took about two weeks.

You WILL need a Tax Id number for your LLC, so it’s easier to pay the attorney to file it for you than for you to do it yourself (IMO). It’s also easiest to name your LLC: FirstName LastName IRA LLC. That way when you go to the bank, they immediately see the relationship. You can also pay for a DBA (doing business as fictitious name) but I didn’t opt to. I highly recommend using an “e-book” rather than a traditional printed binder.

You can also pay for the attorney to be your registered agent within the state of registration (which should be your state of residence). This makes a lot of sense when you’re investing in real estate and there may be legal issues with subcontractors or tenants, but I’m not sure it’s such a great deal if you’re just buying Bitcoin. (Update: the major reason to do this is that if you are the registered agent, and you use your home address, then it’s going to show up in public records.)

It’s absolutely imperative that this be set up correctly, so use an attorney that specializes in IRALLCs, and not just any ole attorney or LegalZoom.

A couple weeks later you’ll get an e-mail with several things.

Articles of Incorporation where the attorney filed your LLC with the State

An LLC seal

An LLC membership certificate

Your Tax ID number

And your LLC Operating Agreement, Minutes, and Ledger

Step 2b: What do you do with all this LLC stuff?

First you need apply your company seal to the Membership Certificate. There are instructions on how to do it using Adobe Acrobat.

Then print out the Certificate and sign it.

Print the signature pages from the Operating Agreement and Minutes and sign them. Scan everything back together and assemble the documents into one big file. (Or print them all and then just scan them together.)

Send them all to your IRA Custodian (see Step 3 below)

Step 3: Tell your IRA Custodian to invest in your IRA/LLC

This will likely involve several forms. You’ll need to to fill out an LLC agreement form where you tell them the name of the LLC and provide all of the documents above, and then an Investment Authorization “Kit” (series of forms) authorizing the IRA Custodian to “invest” (send money) to the LLC. This means that you’re going to have a bank account in the LLCs name. For some odd reason, neither of the self-directed custodians would allow me to simply wire money to an exchange. They required that I wire the money to a bank account first, and then send the money from the bank account to the exchange.

Now…good luck finding a local bank that will open a business account for your IRALLC. They want to know things like what is the nature of the business? How many customers do you have? What demographics do they have? What is your average revenue per month? How much do you anticipate in monthly cash deposits? Uh…It’s a business where I’m going to open the account, send the funds to an exchange, and just keep the minimum balance required to keep the account open. I have no customers and no revenue…

Apparently, even more traditional businesses held in IRALLCs run into this problem. I’ve discovered there are a few banks that cater to the IRALLC market. Solera National Bank is very IRALLC friendly, has no minimum balance requirement, and no monthly maintenance fees. They were very easy to work with, and I recommend trying them based on my experience. You’ll need to answer some questions about the business and send them all your LLC documents, and then wait for it to be approved. This took about a week, (after thrashing around looking for a bank that would take my money), so start your bank account as soon as you get your LLC docs.

Bank Secrecy Act (Currency and Foreign Transactions Reporting Act)

As part of opening the bank account, they’ll ask you a series of questions required by the Secrecy in Banking act. One of them includes whether you are creating or exchanging virtual or digital currency. To the best of my reading, the answer is no. (If you answer yes, they won’t let you open the account by the way.) DISCLAIMER: I am not an attorney, nor do I play one on TV, nor did I sleep in a Holiday Inn last night. This is not advice nor a legal opinion. The best that I can see is that if you’re in the business of exchanging (like Bittrex or Coinbase) or you’re going to be creating a cryptocurrency (like Ripple) then you probably should say yes. But if you’re just buying, holding, and selling cryptocurrency, you should be okay saying no.

Step 4: Open a Corporate Crypto Exchange Account

This is actually one of the hardest steps. BinanceUS and Coinbase are both incredibly obtuse. First they will ignore your application for two to three weeks. Then they’ll ask for more information and ask a huge number of questions that you’ve already answered. They can’t seem to figure out that the source of funds is your own personal IRA money. They seem to think that you’re going to be soliciting other people’s retirement accounts. Honestly, I wouldn’t even try.

Uphold was relatively easy to set up, but their fees are insanely high, and a lot of the crypto can’t be sent anywhere. And then a week later, they told me they were going to suspend my account if I didn’t send them more information that I had already sent them twice. 0/10, would not recommend.

That leaves Gemini and Kraken. Kraken approved me so fast that I never even completed Gemini’s application process. Now I hate Kraken’s interface. It’s even worse than Coinbase (I still don’t understand why they killed Coinbase Pro.) Kraken also doesn’t allow ACH transfers. You’ll have to wire the money. BUT that’s a small price to pay for actually having a working, bona fide corporate account.

Final words

Be very careful NOT to engage in any prohibited transactions. If you’re audited (the IRS says that it’s targeting IRA/LLCs), your IRA could lose IRA status forever.

The IRA will need to pay an annual registration fee with the state you incorporated in, so save some money for that.

You’ll also need to reserve some money for the IRA account fees, and Bank account fees (or maintain the minimum balance to avoid the fees).

You’ll need to provide an annual valuation of your LLC to the custodian that is prepared by a qualified third party (i.e., NOT you or a direct relative).

Overall the process is not that hard, but if you don’t know what to expect or what the right words are, it’s easy to feel stupid and lost.

Dealing with Nick Spradlin was very easy and quick despite my not paying for the expedited service. I’m not sure if he works in all states, but I know he advertises in Florida and Texas.

In this video I explain how to set up a basic budget in a spreadsheet such as Excel or Google Sheets.

You can find a link to the Budget Spreadsheet Template and make a copy for your own use.

Okay, you’ve decided to take the big plunge and invest (or speculate) in the wild world of cryptocurrencies. The potential rewards are overwhelming but so are the choices. In this article, I’ll be covering the major strategies (as I see them) and what is involved. In part 2, I’ll be going over some specifics of how to implement some of the strategies below. Note: Mining is not included in this article as I touched on it in my Beginner’s Guide to Cryptocurrency.

Motivation and Goals

The first question to answer is what is your motivation and what are your goals? Are you just looking to earn a little extra or are you trying to save up to put your kids through school? Your individual situation will influence which strategy might be best to take.

The FOMO is real

In case you’re not up on your internet lingo, FOMO stands for Fear of Missing Out. Although FOMO might have its place (for example motivating you to learn about this stuff in the first place), if you make your investment and speculations based on FOMO, then you’re going to sell low and buy high and lose your shirt. Sometimes it’s better to just hold and wait for another opportunity.

Satoshis or Dollars or Something else?

Is your goal to accumulate satoshis (1 millionth of a bitcoin) or dollars. Trying to do both at the same time may lead to compromises that result in neither. Satoshi gatherers usually have a longer term view thinking that eventually cryptocurrencies will become a viable (if not dominant) way of buying goods and services. Dollar accumulators want the value of their investment to be worth more dollars even if it costs them satoshi value in the short term. Decide on a goal up front.

Strategy 1: The HODL

This comes from a famous misspelled forum post from back in 2013 that reads in part, “I AM HODLING. I type d that tyitle twice because I knew it was wrong the first time. Still wrong. w/e. BTC crashing WHY AM I HOLDING? I’LL TELL YOU WHY. It’s because I’m a bad trader and I KNOW I’M A BAD TRADER.”

The strategy is pretty simple. It’s basically Jeremy Siegel Stocks for the Long Run applied to cryptocurrencies. Choose a selection of crytpocurrencies that you think may have a future, and HODL them for all you’re worth through thick and thin. You probably want to hold some mainstream (Bitcoin, Litecoin, Dash, etc.) as well as some newer, cheaper, up-and-coming alt-coins.

This strategy probably the best one for people with limited time and tolerance for anxiety. Once you buy, don’t look at the price on a weekly, daily, hourly basis. Just check once a year. This strategy is also best for a longer time horizon.

Strategy 2: Sleep at night speculation

This is similar to the HODL strategy except that whenever a coin doubles whatever you put into it, you withdraw half and put it into another potential up and coming alt-coin. As an example, let’s say you buy 100,000 PurplePill coin for the equivalent of $0.001 (total of $100). The price of PurplePill goes to $0.002, now your PurplePill is worth $200. Sell $100 of it and use it to buy another new alt-coin.

If the PurplePill becomes worthless, you still have $100 in the new alt-coin. If the price of PurplePill goes up to $0.1, then your initial $100 is now worth $5000.

But if you hadn’t sold, then it would be worth $10,000!!! This strategy sucks!!!

The FOMO is real. Yes, you halved your potential profit, but you also preserved your original capital, and own a new alt-coin that might do just as well.

This has a couple of benefits over the HODL.

Over time your portfolio will become highly diversified.

This will limit your potential for catastrophic loss

AND put you in a position where you own lots of alt-coins which may one day breakout and make you “instantly” rich after you held them for however many years.

Strategy 3: Day trading

Just like it sounds, this involves frequent trading in and out of various alt-coins. People who do this are usually skilled in the dark art of Technical Analysis. It doesn’t take a huge effort to learn how, but boy can you lose your shirt fast if you don’t know what you’re doing. You can combine this with Strategy 2 to provide a short term and long term combined strategy.

Strategy 4: Masternode investing/speculating

Dash was the first coin to implement masternodes. These are computers that hold a large number of coin (1000 in Dash’s case) and are used to verify and speed transactions. In return, masternodes receive “interest” in the form of new coins. As of this writing, a Dash masternode receives about 200 new Dash each year, representing a 20% annual return on the initial investment.

Sounds like an awesome deal right? Plus if the price of Dash rises, the value of both your masternode and its interest rises. Unfortunately, at the current price of Dash, a masternode will set you back a cool million dollars. If you had bought your masternode just 12 months earlier, it would only have cost you $12,000.

This is the closest to true value investing (IMO) because you get an income as well as a speculative assest (even if you’re being paid in said speculative asset).

So the key is to look for solid up and coming coins that have the potential to go up in value. Good luck.

As a more speculative play, you can look for brand new coins that often pay out more than a 1000% interest. These will pay back the original cost of the coins within 15-40 days. So if the price can hold out for one month, you’ll have your initial investment back plus a masternode in that coin. Keep it or cash out and repeat.

Do this strategy over and over with various new coins. After 1 year of this, you’ll have 6-10 masternodes providing an interest return in that many new coins. Now if just one of them doubles or quintuples in value…. well, you get the idea.

Personally this is my favorite strategy. It does take a little server administration know how to set up a masternode, but you can learn it or outsource it fairly easily.

Warning!! Danger Will Robinson!!!

NEVER NEVER NEVER put your coin in a wallet on the masternode. Never give anyone the private keys to your wallet. Your wallet should reside on your own computer, and the masternode just references the wallet. People have been scammed out of their coin by people they hired to set up their masternode. Don’t fall prey to it.

Bonus: How to evaluate a cryptocurrency

No matter which strategy you adopt, you need to be able to analyze a potential alt-coin investment. Here is a handy checklist that you can use to evaluate the worthiness of a potential investment/speculation.

What are the coins fundamentals?

What problem is coin or project trying to solve? How is their approach different?

Does the project have a compelling story?

Who is on the team? A 30 person team with experience is more credible than a project of 2 people with no experience.

Who is the leader of the team.

What partnerships does the project have in place? It’s one thing to claim a future benefit to…someone. It’s another thing to have a client signed up in advance.

What is the community response to the project?

How much capital is backing the project? Technology is wonderful but without capital to back it up, there’s no there there.

Are there any anticipated events (such as the CEO being featured on a cable news show)?

Technical aspects

What exchanges is the coin listed on? This can dramatically affect the ability of the someone to acquire the coin.

What is the volume of trading? Be very very wary of purchasing coins with low volume. You might not be able to sell it at any price.

It’s practically impossible to ignore Bitcoin and Cryptocurrency lately with the media touting as the largest bubble in the history of the world…even bigger than tulip mania!!! But finding hard facts can be difficult. When you look on Facebook, Youtube, and Google, it seems that 90% of the content is trying to sell you on some kind of get rich quick scheme.

So this little (okay probably not so little) article distills the basics right down to earth in a language that everybody here can easily understand.

So what exactly is a Bitcoin?

At its core, Bitcoin is a distributed ledger system. Thousands of computers all over the world keep a copy of the ledger, which makes it extremely difficult to counterfeit. This distributed ledger system technology is known as the Blockchain. “Owning Bitcoin” is basically owning the ledger entry. In order to record new transactions into the ledger, computers have to solve very difficult math problems.; this is called mining.

As their reward miners get a small percentage of transactions. Addionally mining will occasionally result in a new Bitcoin being discovered. The math is set up in such as way that the problems become progressively harder so that there will be that there will only be 21 million bitcoin ever created/discovered. Early on, it was relatively easy to mine them, and individual miners could mine multiple bitcoin. Now the math is so complicated that most mining is done in “pools” with multiple miners sharing the resulting Bitcoin.

21 million doesn’t seem like it’s enough.

Luckily Bitcoin is fractional, which means that you can own as little as 0.00000001 Bitcoin. (Just like you can own one dollar, or 0.01 dollars (aka a penny).

Where does Bitcoin get its value?

Like all economic questions, the answer is both simple and complicated. I’ll keep this short and dedicate an entire article to it later. The simple answer is supply and demand. As seen above, there’s a limited supply. So where does the demand come from? Well, Bitcoin is useful for keeping track of who owns it, and it can’t be artificially inflated like a traditional government-issued fiat currency (dollars, Pesos, Cruzeiros). Bitcoin set out to be a better and more secure currency than traditional government-issued money.

If you think about your bank account and credit cards, dollars for the most part today are just computer entries of who owns them or who owes them. The problem is that nothing prevents the government or Federal Reserve from just creating additional electronic entries out of thin air. In fact, this is how the banks were bailed out in the 2008 Financial Crisis. Let’s hear it right from the head of Federal Reserve (at the time) Ben Bernanke:

The U.S. dollar has lost 95% of its purchasing power over the last hundred years due to money creation by the government, and it’s considered a bastion of stability compared to the Thai Baht, Mexican Peso, Argentine Peso, Brazsilan Cruzeiro…uh Cruzado…uh New Cruzeiro…uh…Real. You see the point. The demand isn’t just from Americans; the demand is international, partly as a hedge against inflation, and partly as a way to get your money across borders. Bitcoin can be sent anywhere in the world in a matter of minutes.

But isn’t Bitcoin a bubble?

Yes and no. The spike in demand is creating interest that in turn fuels additional demand as speculation. But there are so few bitcoin in the world compared to the number of people who may want them, that it’s hard to say what will happen in the long term. My best guess is that Bitcoin has a long way to go up before it comes down. There will be dips and corrections along the way to be sure, but unless Bitcoin is hacked (unlikely given its nature and track record) or the development team does something really stupid, chances are good that it will remain a valuable commodity for a while. There are some issues with Bitcoin that may limit its ability to be used for every day transactions (see below), but I think that it will still be used for larger transactions and wealth transfers.

Ultimately, the “bubble” exposure is good for Bitcoin and other Cryptocurrencies as the news coverage exposes people to them (and impells me to write articles like this). The more people know about it and own it, the more likely people are to begin using them for transactions, which will turn stabilize the pricing and preventing a future crash.

So what’s a Cryptocurrency?

Let’s sum up first. Bitcoins are ownership of ledger entries in a distributed blockchain. The process of discovering new ledger blocks and verifying new entries for existing blocks is called mining and based on solving complicated math problems. So…those really hard math problems? They’re based on codebreaking, aka Cyrptography.

Bitcoin was the first “currency” to use blockchain technology. There have been several others that are based directly off Bitcoin or developed their own similar (but different) approaches. Collectively these are call Cryptocurrency. Because it’s the oldest and most well-known, it’s become the de facto standard, and all the others are called alt-coins.

Some of the alt-coins are just competitors to Bitcoin that seek to eventually become the most used by addressing problems that bitcoin has. Others just hope for a piece of the action. And some are trying to do something completely different such as become a way to track real estate deeds or educational transcripts or which websites are most trusted.

Some of the most popular alt-coins include:

Litecoin: is essentially bitcoin 2.0. It was designed to be a faster, cheaper Bitcoin. It’s probably technologically superior in every way. It currently serves as a testing ground for Bitcoin development. The Bitcoin developers can see how a proposed solution to a problem plays out in the real world before deciding whether to incorporate it into Bitcoin.

Ethereum is actually a blockchain development platform. It’s main purpose is to serve as a base for potential applications of blockchain to do interesting things.

Dash is designed to be a cheap, fast, and anonymous (if desired) currency for making transactions. The Dash team is heavily marketing themselves. They’ve been targeting the medical marijuana community, since many banks will not do business with them.

Zcash is supposed to be a cheap, fast alternative to Bitcoin.

Monero emphasizes complete anonymity.

You keep saying cheaper and faster. What do you mean by that?

Remember that miners get a fee for verifying transactions (new ledger entries). In Bitcoin, new entries are recorded every ten minutes. To be confirmed, you need at least two separate blocks to show your entry (to prevent double spending of the same Bitcoin). This means that it takes about 20 minutes to get confirmation of a transaction. That doesn’t really work for instant transactions like paying for a cup of coffee, but it’s a heck of a lot better than waiting three hours for a wire transfer or 3-5 days for an electronic funds transfer (EFT).

Furthermore, each block can only record so much information, which means that your transaction may not be recorded in the next block at all. To ensure faster processing, you can offer a larger mining fee. Alt-coins that want to be cheaper and faster have different ways of addressing these two big problems with Bitcoin.

Many people predict that as a result of these issues, eventually Bitcoin will become used as a store of larger wealth, while another alt-coin will be used more for daily transactions.

Stick a fork in it.

When a proposed change to Bitcoin or another Alt-coin is disputed, sometimes the coin will fork. This means that it becomes two separate coins with two separate block chains. As an example, recently there was a dispute over the way to solve some of the issues listed above. So some of the Bitcoin developers forked the Bitcoin project, and called their new coin Bitcoin Cash. When this type of fork happens, if you own some bitcoin, you end up owning your original Bitcoin and the new coin too, so don’t fear the fork.

Okay, so how do I get my mitts on some Bitcoin?

There are essentially three (and a half) ways to obtain Bitcoin. (These will apply to pretty much all of the alt-coins to some degree).

The first is to mine it as described above. (The half is to mine another cryptocurrency and then exchange it for Bitcoin). I have a tutorial on how to get started mining the easy way, so if this interests you, then click here for the tutorial.

The second is to take Bitcoin (or other cryptocurrency) as payment for goods and services. This is actually remarkably easy. Bitcoin is probably best used for someone you know and trust, because of the speed of transaction issue. Another coin that is faster would probably be better for a one-off transaction like buying something off Craigslist. It’s as simple as having a QR code that the person paying scans, enters the amount, and presses send. Even easier than Venmo. Use Google to find local groups. For example, in West Palm Beach, there are number of Bitcon Meetups.

The third way to obtain Bitcoin is to buy it with dollars. The easiest way to do this is with Coinbase. Coinbase is criticized in the Cryptocurrency community (sometimes unfairly, see below), but it’s still the easiest on-ramp to Cryptocurrencies. You sign up for an account, and then you can buy Bitcoin, Litecoin, or Ethereum with either a credit card or electronic fund transfer from your bank. Once you own some coin, transfer it to your own wallet (see below).

Tell me what’s wrong with Coinbase?

The unfair complaints have to do with privacy as Coinbase complies with IRS regulations that govern financial institutions. That’s what allows them to take dollars in the first place.

Other complaints include that it’s relatively slow and the fees are higher than other services. This is somewhat true, but it’s still the easiest way to acquire some Bitcoin.

Finally, the Bitcoins held in Coinbase are not actually held by you. They are held by Coinbase on your behalf. So if something happens to Coinbase, it’s possible that someone could abscond with your bitcoin, but it’s certainly no less secure than Equifax or Target.

One last complaint is that their website “keeps breaking.” This is primarily due to the overwhelming increase in demand in recent days. They are working to try and resolve these issues as quickly as they can.

Recommendations for dealing with Coinbase (and pretty much any online exchange)

Use my link to sign up. Once you buy $100 worth of any coin, we’ll both get $10 of Bitcoin.

Enable two-factor authentication. (When you sign in, they will require verification that it’s you via your phone.)

When you place your order, the price is locked in even though it takes about 5 days for electronic funds transfers to process.

Once your funds have cleared, transfer your coins to your own private Bitcoin wallet.

What’s this about a wallet?

Bitcoin is “owned” by being recorded to a particular Bitcoin address (series of letters and numbers). A Bitcoin wallet generates an address (or multiple addresses) and calculates how much bitcoin is recorded to each address to generate a spendable balance. When you pay someone, your wallet authorizes the transaction.

The magic is contained in a pair of keys, called public and private keys. The private key verifies that the transaction is being generated by the rightful owner of the address. As such, you need to guard your keys. If someone has access to them, they have access to your bitcoin. If you lose them, then you lose your bitcoin!!!

I can lose my Bitcoin? This doesn’t sound very secure.

Well, it’s certainly not idiot proof. But it’s not all that insecure as long as you’re careful. Your wallet will generate a seed, a code or series of words that can be used to regenerate the private key. For the love of God, protect this code. That way, if you lose your phone, or someone throws you in the pool, the bitcoin stored in your phone’s wallet won’t be lost.

One other thing to be aware of is that if you’re dealing with multiple currencies, don’t send the wrong currency to the wrong. For example, if you send litecoin to a bitcoin address, there’s a good chance that they’ll be lost, possibly forever.

Wallet Practices

Choose a secure wallet, such as an offline wallet to store the majority of your Bitcoin. Then transfer a little bit to an online wallet (whether your phone or computer) for walking around money. If you practice this protocol, if you do ever lose your online wallet or have your computer hacked, you might lose the small amount stored there, but you won’t lose your savings.

The most secure wallets are called hardware wallets. They are typically a USB device that runs the wallet software and authorizes transactions. Since the private key is stored in the device, when it’s unplugged there is no chance that anyone can electronically still your Bitcoin. Make sure you configure a passphrase for the hardware wallet to prevent someone who finds your hardware wallet after if fell out of your wallet from taking your bitcoin. Keep the seed separate from the. The Ledger Nano S seems to be the most popular hardware wallet at this time. The Trezor is never in stock and is a bit more expensive. The Keepkey is another alternative.

You don’t need a hardware wallet, so don’t let that stop you from getting started. You can also create a paper wallet for free.

You need a wallet for each currency you want to own.

Some wallets are called Multi-Wallets because they can handle multiple crytpocurrencies. Others are specific to a single type of coin. Before you buy a hardware wallet, make sure that it can handle the currencies you want to use.

Two popular software multi-wallets are Jaxx and Exodus. Jaxx can be used on your phone and computer. There are some security concerns with the way that it stores your private key, so don’t go doing stupid things like getting a virus, and see Wallet Practices above. One of the nice things about the Jaxx wallet is that it integrates Shapeshift, which is an exchange for Cryptocurrencies. So say, you have Litecoin in your wallet, but the person you’re buying from wants Dash. The Jaxx wallet can convert it for you via Shapeshift, and then send the Dash. Exodus also integrates with Shapeshift, but is not available for phone and tablets.

Bottom line: Take Action Now

I’ve know about Bitcoin for at least 7 years. I kept thinking, you know, I should figure this stuff out and buy some…maybe $500. If I had done that back in 2010 or 2011, or 2012, I’d be a millionaire. If I had even done it in early 2017, my $500 would now be worth about $8000. It was the inertia and learning curve that did me in.

I don’t know what the future holds specifically, but I can tell you that blockchain technology is going to revolutionize the way we do business and make purchases. Chances are very good that Bitcoin will continue to rise in value along with some other alt-coins.

It’s not too late. There’s still a lot of up Bitcoin before there’s a down. But don’t be stupid. Start small. Learn how it works. Become familiar with the issues. Then you’ll be prepared for what comes.

So, here’s your homework:

Follow my Minergate Quick Tutorial, and you can be mining cryptocurrency in about three minutes.

Start a Coinbase account and buy a small amount of crytpcurrency (Bitcoin or Litecoin). Whatever you’re comfortable with, whether it’s $5 or $500.

Go out to lunch with a friend. Have them pay in dollars and you pay them in Bitcoin.

Use Google to find other local people who use Bitcoin.

Once you’ve done these things, now you’re ready to snatch the rock from my hand and go out into the world. In my next article I’ll lay out some investment and speculation strategies as well as share some resources for learning more.

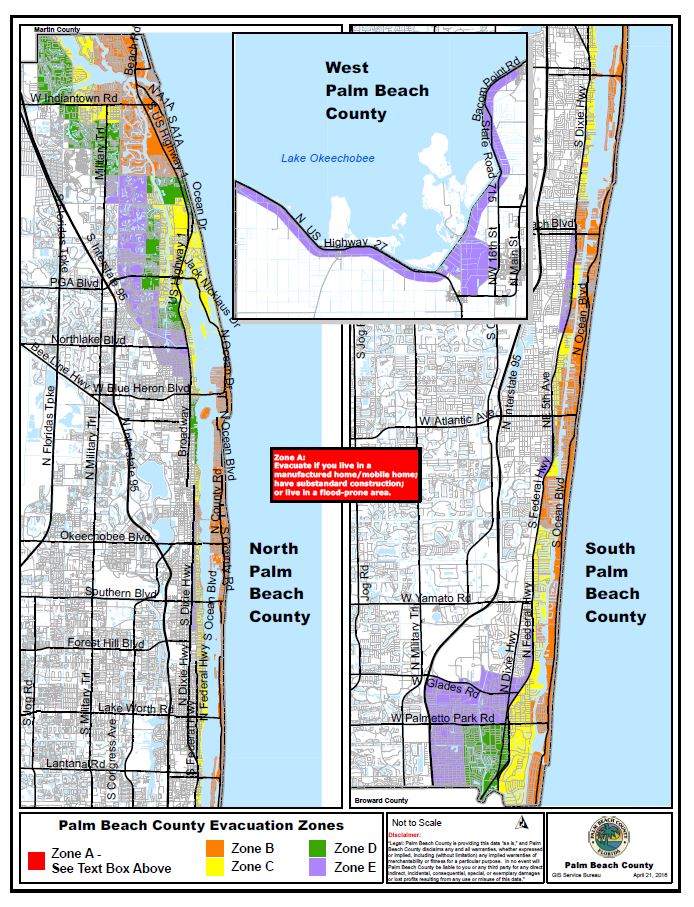

If you watched the news on Hurricane Irma recently, you have been led to believe that the entire state of Florida was being evacuated. In fact, only the barrier islands and a couple blocks inland were evacuated. As you can see from the map below, the actual number of people evacuated is tiny.

Evacuation Map of Palm Beach County

The media would gloss over it, but every now and then the Governor would say, “If you don’t need to evacuate, you should stay where you are.” So the vast majority of Floridians should have stayed where they were.

There is a season for Hurricanes

Unlike earthquakes, which seem to be random, Hurricanes only occur during Hurricane season, usually from September through November. During the Summer, the Atlantic Ocean warms up above 80 degrees Fahrenheit. This creates the conditions necessary for the development of hurricanes.

The nice thing about hurricanes is that you get more than a week’s warning that they’re coming. Now up until this year, most people ignored hurricanes until about 48 hours before they hit. Then there would be gas shortages and people would strip the grocery stores of food and water. This year, with Irma, people started freaking out more than a week before.

The bottom line is that the right time to prepare for a hurricane is before hurricane season. In fact, National Hurricane Preparedness Week is the second week in May. But I know you’re a procrastinator like me, so I’m declaring June 25, Heymanator Hurricane Preparedness day. So let’s look at how you can be prepared to live without power. In this article we’ll talk about some creature comforts: food, phones, and tablets, and fans.

Your Refrigerator/Freezer will stay cold for at least 2 days

For some reason, the vast majority of my friends seem to think that if food has softened at all in the freezer it should be thrown out. So let’s review a little thermodynamics.

Your freezer is usually around 0 degrees F

Your fridge is usually around 40 degrees F.

Water freezes at 32 degrees F AND melts at 32 degrees F.

This means that, if still have a single formed ice cube in your freezer, then your freezer did not go higher than 32 degrees, and your food is safe! On average, an unplugged refrigerator should keep cold for about 2 days.

Even if you have a generator, you don’t need to run it 24/7. Running it for 2 hours twice a day should be enough to keep your food perfectly cold.

Strategies to make the most of your Fridge/Freezer

Before the storm

If you have a lot of space in your freezer, fill up jugs or bags of water and freeze them.

Identify items that can be sacrificed in case of power failure (for example that ham hock you’ve planning on making into soup for the past 2 years.)

Get out some old blankets. Once you lose power, you can put them on top of the fridge to insulate it.

After you lose power

Take the ice cream out of the freezer and eat it.

Put your milk and other easily spoilables into the spot in the freezer opened up by the ice cream.

Cover up the fridge with the blankets to increase its insulation.

You don’t need a generator

If you have a car, you already have all the generator you need to power your refrigerator (and charge your cell phone and tablets). All you need is an inverter. The average energy star refrigerator will draw somewhere between 150-200 watts when running, but takes 750-800 watts when starting up.

SO… you’ll need at least a 400 watt inverter (most inverters can handle a surge double their rating, although YMMV), but it’s safer to go with an 800 watt inverter. The important thing to remember is that a car’s cigarette lighter socket will only allow ~150 watts to be drawn. Try to run your refrigerator through it, and you’ll likely blow a fuse. Instead, you’ll need to use alligator clips to attach the inverter directly to your battery.

But before we get to the nuts and bolts, let’s talk generalities. An idling car or SUV uses about 0.2-0.5 gallons of gas per hour. So if you run your car for two hours twice a day to power your refrigerator, then you’ll use between 1 and 2 gallons of gas. This isn’t quite as efficient as a dedicated generator, but then again, it’s a heck of a lot cheaper to buy a $50 inverter and make $15 cables than even the cheapest generator.

And you can take the inverter with you on your next road trip and use it to do all sorts of fun things in the car like let your kids play Xbox. Or make coffee while camping because you were too lazy to learn how to use a French Press. And let’s not forget that an inverter is much smaller and easier to store than a generator.

So, after the storm passes you by, you…

pull your car out of the garage,

pop the hood,

leave the car running,

connect your inverter to the battery using the cables,

While you’re at it, maybe you should charge up your iPad, Kindle, phone, and maybe your laptop too.

Heck run some fans to help keep you cool maybe this cheap personal fan running 35 watts max or this whole room Vornado fan running 65 watts max.

When you’re done running your refrigerator, you can unplug it, turn your car off, and keep charging your cell phones and ipad.

Note: when running your refrigerator, take the covers off. Then put them back on when you’re done.

What Inverter should I get?

Pro tip: get a 1×4 that’s long enough to lay across the hood of your car/suv. Then mount the inverter to the board. Wrap some old t shirts around the ends of the board to protect your car’s finish from the board and prevent it from sliding. Now when you need to use the inverter, you won’t have to balance it on top of the engine. You just lay the board across the car after opening the hood.

What kind of inverter should you get? Steven Harris (whose advice much of this article is based on) recommends the following brands/models. He particularly likes the Whistler because supposedly it can handle double its rated power draw for up to 10 seconds. But it’s a little pricier. Yes, these are the same brands that make radar detectors.

Note that when using 800 – 1600 watt inverters, you’re going to need to use much heavier gauge wire and keep the wire as short as possible (<3 feet). Either 0 or 2 gauge wire is recommended for 1600 watts, and 0 gauge if you’re going above 1600 watts. It’s cheapest to buy the wire by the foot from Lowes or Home Depot, and then put ring connectors on them yourself (or buy something like this). None of the 800 watt and up inverters listed come with wires.

Bestek 300 watt inverter. This inverter is cheap and might run your refrigerator, BUT, you’ll need to buy a car adapter kit to clip it to your battery. So once you figure in that expense, you might as well just get the more expensive 400 watt inverter, which includes the clips.

Cobra 800 watt, Cobra 1000 watt, or Cobra 1500 watt inverters. Note that the 800 watt version doesn’t have a display to show how many watts are being drawn. The 1000 and 1500 watt versions do.

Whistler 800 watt or Whistler 1600 watt inverter. Supposedly the 800 watt comes with cables but has no display. The 1600 comes with a display and no cables.

Can you please sum this up? tl;dr

Get an 800 to 1600 watt inverter

Get a heavy duty extension cord (without lighted ends is better if you’re planning on using the inverter with the car off.)

Run your car for 2 hours and use the inverter to power your stuff.

Start the refrigerator first by itself because it draws more power when starting up.

Once it’s running you can plug your other stuff in.

After 2 hours, unplug the refrigerator and

Note: you can use this method to run your TV and Cable box too but ONLY do that when the care is running.

In the next installment of this series, I’ll talk a bit about generators.

Acknowledgements.

I first learned about this technique from The Survival Podcast interview with Steven Harris.

The Amazon links in this article are affiliate links, and if you buy through them, I’ll get a small commission. If you’d prefer to support Steven Harris instead of me, you can go through his links at Solar1234.com or you can support Jack Spirko (The Survival Podcast) by buying through his Amazon links.

In the last few posts, I’ve talked quite a bit about how I’ve lost weight (31 pounds as of today). I’ve gone into some detail about the diet, but I haven’t really talked about the workouts much. There’s a couple reasons, but the main two reasons are 1) workouts are complicated, and 2) 95% of your results will come from your diet. There’s a reason fitness models say, “abs are created in the kitchen.”

I do plan on writing more about the workout in the future, but for today, I just wanted to give you some tips on how to do more chin ups (or pull ups if you desire). When I started this journey 14 weeks ago, I could barely do 4 chin ups or 3 pull ups. This Monday I did 5 chin ups with 40 lbs attached followed by a set of 6 chin ups with 25 pounds attached. Today (Thursday, I did a set of 13 bodyweight chin ups).

Now I know for some people that may not sound very impressive, but I haven’t been able to do more than 8 pull ups or chin ups since I was 19. And I certainly wasn’t as explosive as I am today. So here’s how I did it. You can use this method with either pull ups (palms away) or chin ups (palms toward you). Personally I prefer neutral grip chin ups (palms facing each other). For the rest of this article, I’ll just call them pull ups out of habit.

Some people will tell newbies that they need to be able to do 8 pull ups or 12 pull ups or even 20 pull ups before they start adding weight. But I prefer to start adding weight as soon as you can do 4-6 pull ups. I’ve never been good at doing lots of pull ups, and if I had waited until I could do 12 pull ups before adding weight, I’d probably still be doing 5 pounds. Below is how I did it, and you can too…if you like.

Step 0: Be able to do at least 4 pull ups

If you can’t do at least four pull ups, then that’s your first step. If you can’t do any pull ups, then follow this below video for a nice progression. If you can do at least one pull up, then do several sets of as many as you can do with good form at least three days a week.

Step 1: Add 5 lbs

Once you can do a at least 4 good pull ups, it’s time to add some weight. Get a dip belt. Attach 5 pounds and do a set. Wait at least 3 minutes, then do a second set bodyweight pull ups. On your other two workout days just do one set of bodyweight pull ups. So to recap: one set of weighted pull ups and 3 sets of bodyweight pull ups per week.

Note: I was doing this while on a fairly aggressive cut of 700-1000 calorie deficit per day. If you’re eating at maintenance or bulking, you can do three sets on your weighted day or even to two days of weighted pull ups (I’d recommend at least 3 days recovery between weighted sets.)

Step 2: Adding reps

Keep doing the weight you added in Step 1 plus two sets of bodyweight pull ups on other days until you can do 6 weighted pull ups. Here are some tips:

Focus on trying to make your upward movement as explosive as possible.

Try to keep your shoulder blades retracted (pull down and toward each other)

Don’t reach your neck for the bar.

Don’t struggle with half reps. When you can’t complete the rep with good form, don’t do it at all. If you really want to do another rep, jump up to the top and do a long negative (slow descent) or get an elastic band and do assisted pull ups.

Step 3: Add 5 more pounds

When you can complete six good, explosive pull ups, it’s time to add 5 more pounds.

If you can do 5 or more reps with the higher weight, then add 5 pounds again next week.

If you can only four reps with the higher weight, stay at that weight until you can get 6 reps and then add another 5 pounds.

If you can’t get four reps with the higher weight, drop the weight by 2.5 pounds the next week.

Keep doing your bodyweight pull ups for the second set and on your other two days.

Step 4: Add weight to your second set

When you get to the point where you’re doing pull ups with 10% of your bodyweight added, you can start adding weight to your second set. So if you’re 180 pounds, when you get to 20 pounds, add 5 pounds to your 2nd set. Generally speaking you should be able to get at least one more rep out of your 2nd set with lighter weight than your first heavy set.

Whenever your second set gets 2 good reps higher than your first set, add five more pounds to it. Follow the same rules as step 3 (but with a higher rep count).

Step 5: Take videos of yourself doing weighted pull ups.

That’s pretty much it. The video below is my second set of weighted pull ups this week with 25 pounds added. You can see my weight progression in the table below. Notice that even though my weight is going down, the total weight I’m lifting is going up. (So my absolute strength and relative strength are both increasing.)

Date

Weight

Set 1

Wgt w/body

Reps

Set 2

Reps

2/23/2016

196

0

196

6

0

3

2/29/2016

195

0

195

6

band

5

3/7/2016

194

0

194

5

0

4

3/14/2016

195

15

210

4

5

4

3/18/2016

193

15

208

4

5

4

3/23/2016

192

15

207

5

5

5

3/28/2016

192

15

207

5

5

5

4/2/2016

190

20

210

4

5

5

4/11/2016

189

20

209

4

5

5

4/18/2016

188

20

208

6

5

6

4/25/2016

188

25

213

5

5

6

5/2/2016

186

30

216

5

10

7

5/9/2016

186

35

221

5

10

7

5/16/2017

187

40

227

4

15

6

5/23/2016

184

40

224

5

20

6

5/30/2016

185

40

225

5

25

6

6/6/2016

182

40

222

5

25

6

Frequently asked questions:

Man! I could NEVER do weighted pull ups!

It’s not really a questions, but that is exactly what I thought until I started doing it. I’ve never been good at pull ups. When I was in the Air Force Academy, the max I ever did was 13, and I assure you the last five were not nearly as explosive as the last five in my video at the top. When you see someone doing pull ups with 70 pounds attached, you think, “there’s no way I can do that,” and you’re right. You can’t do it…now. But if you start with adding 5 pounds, increase your reps to 6, add five more pounds, rinse and repeat, you’ll be doing 45 pounds before you know it.

So what’s this simple secret you mentioned in the title?

Too subtle, eh? The secret is adding 5 pounds. As you get stronger, you’ll be able to do more pull ups with just bodyweight.

Does this work for weighted dips too?

Absolutely. It actually works even better for weighted dips. In the time it took me to go from 0 to 45 pounds for pull ups, I went from 10 pounds to 77.5 pounds for 6 reps for dips. The only thing holding you back is not using a dip belt. Some gyms even have one you can borrow. But if not, buy one on amazon.

Recent Comments